Justin Sullivan/Getty Images News

Tesla’s (NASDAQ:TSLA) stock has suffered recently with the company’s market cap dropping to less than $900 billion, after pressure from Elon Musk’s Twitter (TWTR) investment and potential stock sales. Investors might be fooled into thinking that this short-term downturn from stock sales represents an investment opportunity, however, as we’ll see, Tesla still remains significantly overvalued.

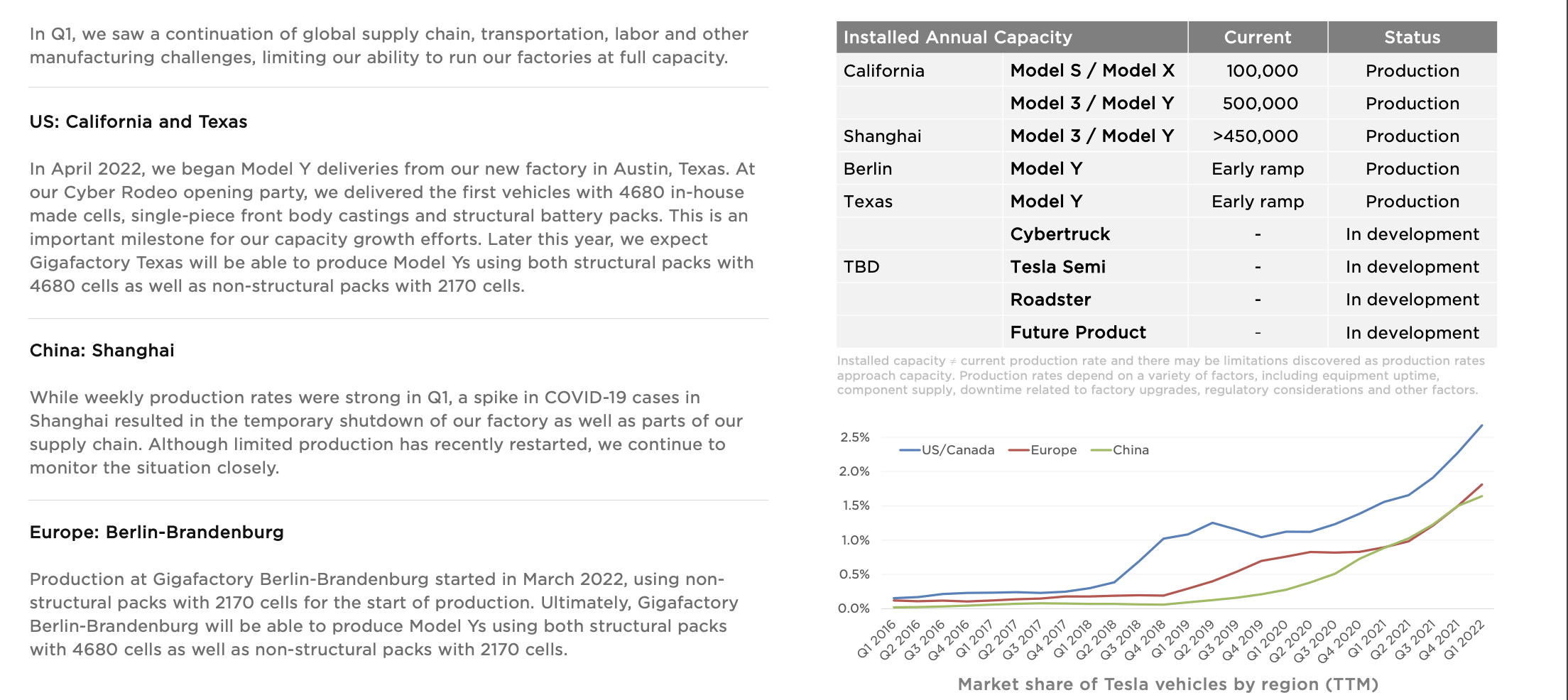

Tesla Volume Ramp

Tesla’s ability to continue succeeding is based on ramping volume and succeeding with new models.

Tesla Volume Ramp – Tesla Investor Presentation

The company has been ramping up volume although its Shanghai factory has suffered from COVID-19 volatility. However, it’s worth noting that the company’s factories and focused capacity for the Model S/X/3 are effectively done. The company could ramp up the Model Y or other future projects, however, it shows the company sees demand for other vehicles as peaked.

An example of this can be seen on Tesla’s website. The cheapest Model 3 has an estimated delivery date of Aug-Nov 2022. The top end has a Jun-Aug 2022 delivery date. The top end Model Y is Jul-Sep 2022. The company’s backlog has decreased substantially from its prior backlogs, and especially with the potential for a weaker market, we see that weakness continuing.

With competition increasing significantly, we view Tesla’s volume ramp as slowing down. It’s telling that the company doesn’t have any new factories planned for its Model 3/S/X.

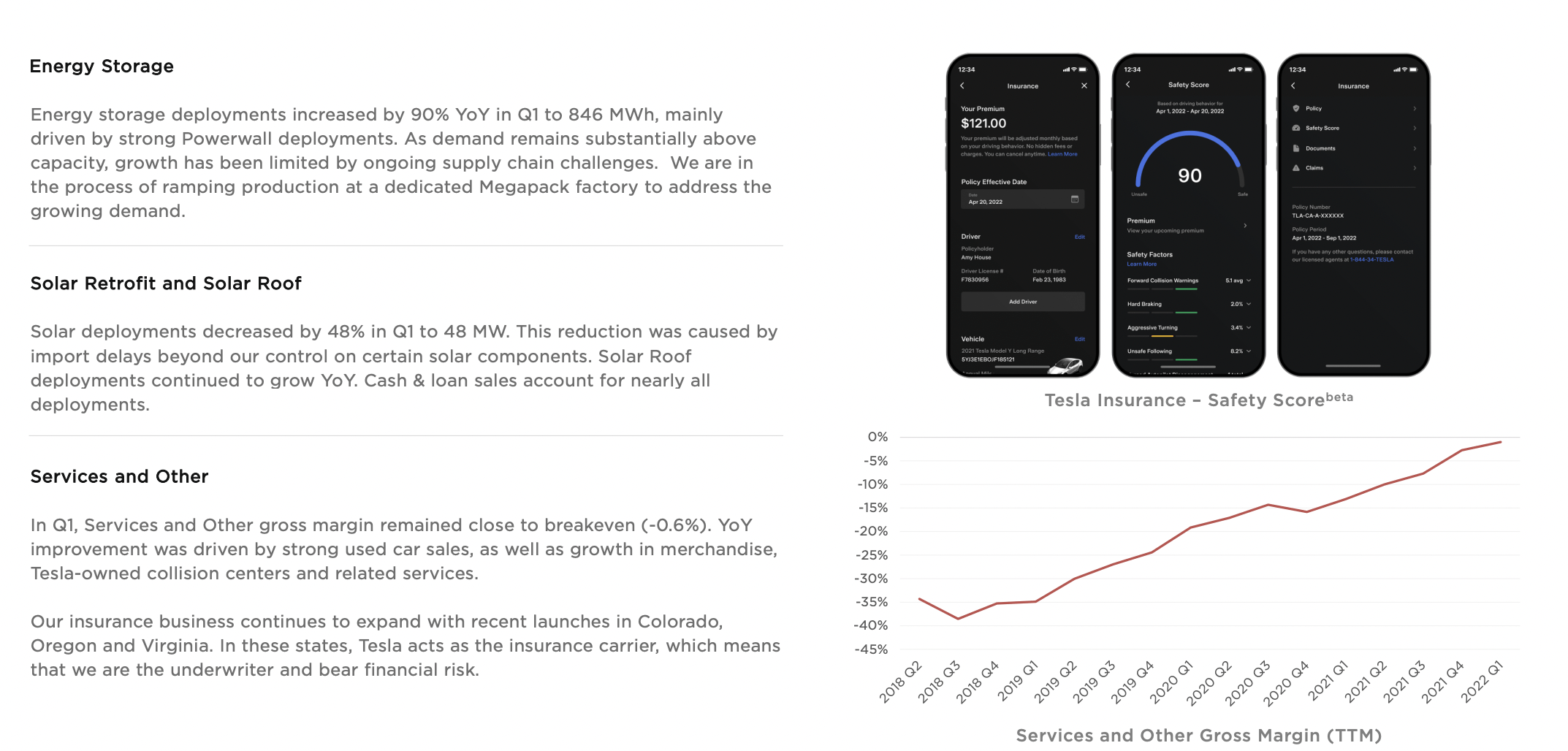

Tesla Energy Storage/Alternatives

Tesla has numerous alternative businesses including energy storage and other alternative businesses.

Tesla Alternative Businesses – Tesla Investor Presentation

The company’s energy storage business is the bright spot in its alternatives business. The company has seen deployments increase 90% YoY. However, the company does have some risks to the business here. First, energy storage is a worse use of capital from a profit perspective versus building cars. Tesla itself has admitted that before.

That means that as long as there’s volume demand for the company’s cars, the company’s energy storage will take a back seat. Second is the company’s solar business. We’ve discussed this before, but this business is negligible. It’s decreasing in size, has a single-digit market share and no competitive advantage.

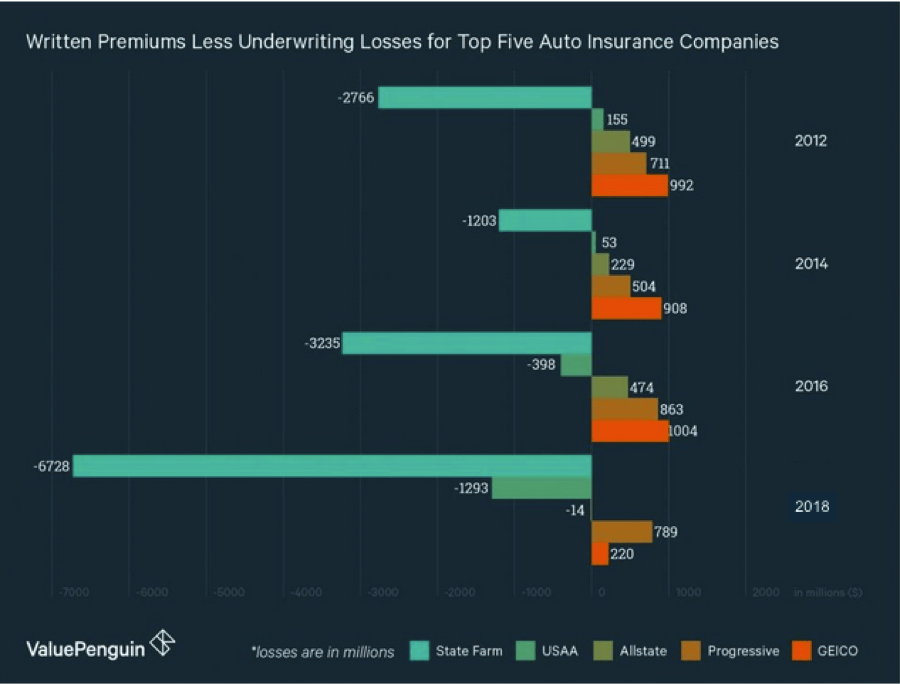

Tesla Insurance

Another development for Tesla is the company’s announcement that it’s launching an insurance business.

Insurance Underwriting Results – PMR Law

Insurance isn’t a high profit margin business. It relies on the generation of the float and the potential investments of the float to generate returns. A substantial insurance business can take advantage of a continuous float to invest and generate long-term returns without a significant negative impact to that float.

The takeaway here is that insurance companies operate off of scale. Travelers is the 10th largest insurance company in the world, insures more than 2 million vehicles. Even with 100% of U.S. Tesla owners getting insurance through Tesla, the company won’t reach that number. More so, even if it did, the insurance business would only be valued at a few billion $ based on peers.

Warren Buffett whose Berkshire Hathaway owns GEICO recently commented they don’t expect Tesla to outperform here, given their data is mostly the same as the current insurers. Here, we believe the opposite is true. Not only will Tesla not outperform but the company could lose money or, in the event of a mistake, hurt a brand. We see three unique downsides for the company.

(1) Multi-line discount. Most major insurers offer to bundle home insurance with multiple cars, home insurance, umbrella insurance, etc. Tesla can’t offer those discounts to customers meaning that offering competitively priced insurance will be more difficult.

(2) Reputation. It’s no secret that Americans hate their insurance providers. Unfortunately, the premise of maximizing profits for the insurer is different from maximizing profits for the insuree. And oftentimes those competing interests come to clash at a tough time. Tesla will need to outperform its customers because of the reputational risk.

Someone who has a bad experience with Tesla insurance might leave Tesla overall. No one buys a different car because they dislike Progressive.

(3) Start Up Cost. Insurance is a crowded market without a high barrier to entry. However, Tesla will be spending substantial money to startup and join the industry. The company will be spending cost with no guarantee of returns, which is a risk for the company’s future shareholder returns.

Tesla and Tech, A Unique Downside

We want to take the opportunity to highlight what we see as a unique risk for Tesla. The company is a massively popular car among tech industry employees. The carmaker has a >10% market share in California versus a 2% market share in the United States. It’s well known in the hub of the technology industry how popular the company’s cars are.

However, we see this as a unique potential downside for Tesla. The company’s cheapest cars clock in at 2x the cheapest car from the traditional low-cost manufacturers (Honda and Toyota) as the company has struggled to meet expectations. Even versus luxury manufacturers such as BMW and Mercedes, the company’s cheapest car is more expensive.

More so, the tech industry has suffered. After leading the bull market for the last 5 years, the market is now down roughly 25%. Given Tesla’s unique positioning to tech industry employees, we expect the downturn will hurt the demand for the company’s products, especially higher end products.

Tesla Isn’t Recession Proof

Tesla has reasonably strong cash and cash equivalents at roughly $18 billion. However, the car industry is incredibly capitally intensive, and losses ramp up significantly during a market downturn.

Through the 2008 recession, U.S. carmakers lost $10s of billions. Capitol obligations can be difficult to avoid in the industry with factories needing to be kept running because the cost of shutting them off is even more expensive. However, that doesn’t mean that they’re making a profit. Tesla hasn’t actually had to face a market downturn yet.

We expect there are two factors here that will again make Tesla less likely to survive a recession.

(1) People cut spending during a recession. Tesla is effectively a luxury brand at its pricing. In 2008, Toyota outperformed. During an upcoming recession, we expect Tesla to similarly underperform in line with luxury brands. They also might be less willing to try the uncertainty of an electric vehicle.

(2) Capital growth. Tesla is focused on growing substantially, and as we saw above, has numerous factories that it’s planning to build. Those capital obligations without production could cause the company to have higher losses than companies only maintaining existing factories. That risk is worth paying close attention to.

Thesis Risk

The largest risk to our thesis is that Tesla is a unique company that has a proven ability to outperform. The company, in many ways, defined electric vehicles as a segment, especially luxury vehicles, and the company’s competitors have struggled to compete. There’s no guarantee that the company can’t continue increasing market share and returns.

Conclusion

Tesla is now 40% below its 52-week highs. The company’s weakness was exacerbated by Elon Musk’s ownership and his pledging of the company’s stock against his Twitter acquisition. That sell-off accelerated as a result of the general technology sell-off in the markets. Despite this underperformance, we see that as just the start.

The company is showing peak demand with no additional factories planned for the Model S/X/3. Most vehicle purchases can see delivery with is shorter delays than other manufacturers’ vehicles such as Toyota’s RAV4. We also view the company’s position in the tech markets as a unique risk to its business model. As a result, we continue to recommend against investing in Tesla.

from WordPress https://ift.tt/OhFCMpu

via IFTTT

No comments:

Post a Comment